Stock Indices: An NDX Primer

In the last few weeks, the (relatively) new DeFi platform Indexed Finance has started getting attention as a provider of passive exposure to portfolios of cryptocurrencies.

I’ve been hanging around in the Discord for a few days now, and noticed that there’s been a pretty significant number of questions about what the various tokens mean, how they’re priced and what they represent. This both excites and depresses me — it means that more people are getting exposed to ‘traditional’ market instruments in a realm that’s accessible to them, but also suggests the existence of a knowledge gap that isn’t being bridged.

—

See also:

—

I thought I’d fix that with a quick post explaining a few things, without going into discussions about governance, swap fees, minting, controller contracts et al. The existing documentation on the NDX page is more than sufficient to cover the details of execution on the day-to-day side of things. This is purely a primer for “What am I getting in to if I buy non-governance tokens on this platform?”.

Whilst I’m effectively anonymous to you (despite using my real name here…), I’ve got a little bit of pedigree to back up what follows: I worked at a major bank in Asia for four years, and have three relevant degrees in the various fields surrounding decentralised finance. With that said, everything you’re about to read is platform-agnostic stuff.

Disclaimer: I hold some NDX governance tokens. However, this is a theoretical look at how indices work in general (with a smattering of discussion surrounding Indexed portfolios that exist at the time of writing), and the performance of said tokens are irrelevant to this article.

What’s An Index?

You know the answer to this already, even if you’re not aware of their constituent components or inner machinations. The S&P 500 is an index. The NASDAQ Composite is an index. The FTSE 100, the Hang Seng, the JSE 40, the NIFTY 50… they’re all indices. These names get thrown around a lot daily. If you’ve got any sort of investment vehicle for your pension, you’re likely in more than one already.

An index is a snapshot of a bucket of stocks. That’s it. The actual contents of the bucket may vary, but they’re used as a single metric to indicate “how has this group of stocks performed over time?”.

The FTSE 100 tracks the health of the top 100 largest companies by market capitalisation on the London Stock Exchange. The S&P 500 follows 500 companies selected by a committee (high market capitalisation is a good indicator, but not a guarantee of inclusion). I mention these two in contrast to each other — one is strictly rules-based, whereas the other has a bit of the human touch to it.

That portfolio of tokens that you’re looking at on Zerion right now? That could conceivably be considered an index if you apply some discipline about what makes it in, and how often you rebalance it (more on this later).

Right now, there are two indices available on NDX, namely CC10 and DEFI5. As for what they represent, it’s exactly what’s written on the tin — CC10 tracks the health of 10 Ethereum-based tokens, and DEFI5 does the same for 5 Ethereum-based tokens that are explicitly dedicated to decentralised finance.

What Goes Into An Index?

When an index is first created, there are a handful of decisions that need to be made regarding it’s inner workings: specifically a) the list of what it’s going to be tracking, and b) the prominence of each member in that list.

For the rest of this section, I’ll use the DEFI5 index pool as a running example. The same fundamentals apply to CC10, and all other index pools that might appear going forward.

There’s also some terminology shadowing here too that’s worth pointing out — the terms index pool and index tracker are the same thing: the former is just indicative of the fact that it’s cryptocurrency that we’re dealing with rather than brick-and-mortar stocks.

The first step in defining an index is determining it’s universe — all of the potential assets which could be included. For the FTSE 100, this potential universe is simply ‘all stocks trading on the LSE’. In the case of DEFI5, the universe was initially determined to be the following:

The rules proscribing that universe are detailed here, but suffice it to say that there are nine candidates at the time of writing.

So why not just have a DEFI9 portfolio? Well, you could — there’s nothing stopping this. However, proscribing the membership of an index introduces a degree of flexibility in that the universe can (and will) expand/retract as time goes on: eventually, one of these tokens will fall out of favour before the others, or another hitherto non-existent token will appear and blaze a trail. By separating an index pool’s universe from it’s membership, we increase volatility but gain the ability to swap out poor performers for up-and-comers.

The next question is: how do we rank the universe to determine which of the above nine make the cut? In this case, it’s just market capitalisation: the number of tokens in existence multiplied by their price. To be more specific, the current NDX pools use fully-diluted market capitalisation — but for the scope of this post, the difference isn’t worth banging on about.

In short, under this ranking mechanism, we can cut down the above universe from nine to five: UNI, AAVE, COMP, SNX and CRV.

How Is An Index Weighted?

Now we know which tokens are going to make it in to the pool, there’s a separate decision to be made about the weightings — the slice of the pie allocated to each constituent member. There are a few ways to do this:

- Equal-Weighted: if there are 10 members of an index, you assign a weight of 10% to each. Indices weighted equally will give equal prominence to giants like Apple and Four Seasons Total Landscaping, and are traditionally (in brick-and-mortar indices) considered higher-risk/higher-return due to the potential for rapid expansion by the smaller companies contained therein. There are a bunch of S&P 500 equal-weighted indices out there, so they’re not uncommon.

- Price-Weighted: if company A has a stock price of $20 and company B has a stock price of $10, the weighting would be split 2:1 in favour of the former. This is the method used by the Dow Jones Industrial Average, and has the benefit of simplicity, but the downside that weights assigned are somewhat arbitrary — two companies might be worth the same amount, but if one has five times as many total shares as the other (and hence the stock price varies by a similar proportion), that difference will be reflected.

- Market-Capitalisation-Weighted: we’ve already talked about this above — weights are determined based on the overall value of the company/token. This is by far the most commonly used weighting mechanism for indices — the ‘normal’ S&P 500 uses it, for example.

The DEFI5 index pool uses a slight variation of this last weighting method — namely square-root market-capitalisation weighting, which allows for a more equitable weighting between members whilst still acknowledging the outsize impact of particularly large stocks/tokens.

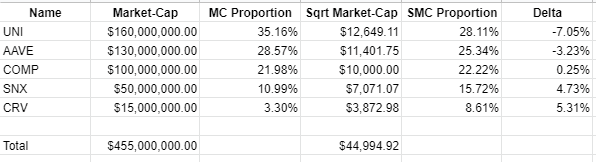

To illustrate, here’s an example breakdown of a theoretical weight-allocation for NOTDEFI5 with some dummy numbers (so please don’t chase me down about how these figures aren’t accurate!):

From the above, we can see that whereas under a pure market-capitalisation weighting, UNI would beat out CRV by an order of magnitude — in a square-root setting, it’s closer to a factor of 3.5. People can (and do) argue about which the best metric is to use for these decisions — I’m not about to tip my hand either way, though.

When NOTDEFI5 was created, the SMC proportions calculated were designated as the target weights for each constituent. If I wanted to go out and follow along with this by myself with, say, a million dollars, I’d go out and buy $281,100 of UNI, $253,400 of AAVE, and so on.

I know I’ve already said “that’s what an index is”, but… that’s a more longwinded way of explaining what an index is. Pick a universe, filter your members, decide how they’re allocated, acquire the underlyings and issue some proxy stock/token.

Why Are Indices Rebalanced?

There’s not much point in buying these things if we’re expecting the price to stay stable, though. The whole reason we’re doing this is because we’re expecting the prices of the components to go up (crypto never goes down, we know this by now). As they do, the weightings of what’s in your index will shift away from their targets.

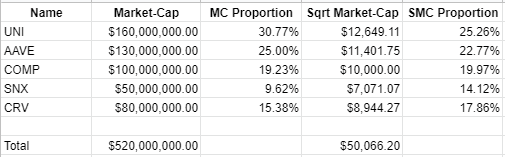

Going back to the above, if CRV went on a massive bull run and suddenly hit a market cap of US$80 million, that’d pretty significantly change the composition of your holdings if everything else stayed stable:

However, whilst these proportions now reflect the current state of affairs for those tokens, the target weights of my index haven’t changed. If I decided to add another million dollars worth of underlyings to my personal NOTDEFI5 index tracker, I would still be purchasing SNX over CRV at a rate of nearly 2:1 (15.72% versus 8.61%) due to the weightings that were set when the index was created: even though, at present, I should really be buying slightly more of the latter over the former.

It’s these underlying changes in fortune that necessitate rebalancing — the adjustment of target weights to reflect the latest market information and shuffling of assets so that your holdings reflect these new weights. These typically happen every three to six months for the indices that you’ve got in your 401(k), but crypto moves fast — the intent for NDX pools is for target weight rebalancing to happen every two weeks, with reconstitution (the updating of which tokens are in the pool) taking place monthly.

The process is pretty much identical to the initialisation step I talked about above — the market caps of the stocks within the universe are scanned, the new members are determined, new target weights are set, and assets are shuffled around to reflect the new composition. If a new token/stock has met the criteria to be included, it must be at the expense of another being de-listed (there’s a lot to be said for the process of phasing out a token from an index pool such as DEFI5, but that’s out of scope).

Finally, Why Hold An Index At All?

So, at the end of all this (or if you just scrolled down)… why hold an index? Fundamentally, this comes down to pure convenience — if you’re bullish on a particular sector, then purchasing an index tracker acts as a proxy that gives you exposure to said sector without having to purchase the constituent stocks yourself, incurring fees (viz. gas, in our context) for each.

In brick-and-mortar land, these have a 136 year history, ever since Charles Dow published his first transportation stock index in 1884.

They work. And if we’re looking to get wider acceptance as an alternative way of investing, they’re something that needs a solid platform. Whilst I’m not going to give a rabid endorsement of something that’s still in it’s infancy, Indexed Finance looks to be on the right track in terms of being a progenitor.

—

Anyway, I hope that helped a bit! If you’ve got any questions, things you’d like me to correct, or requests to clarify things, please let me know.